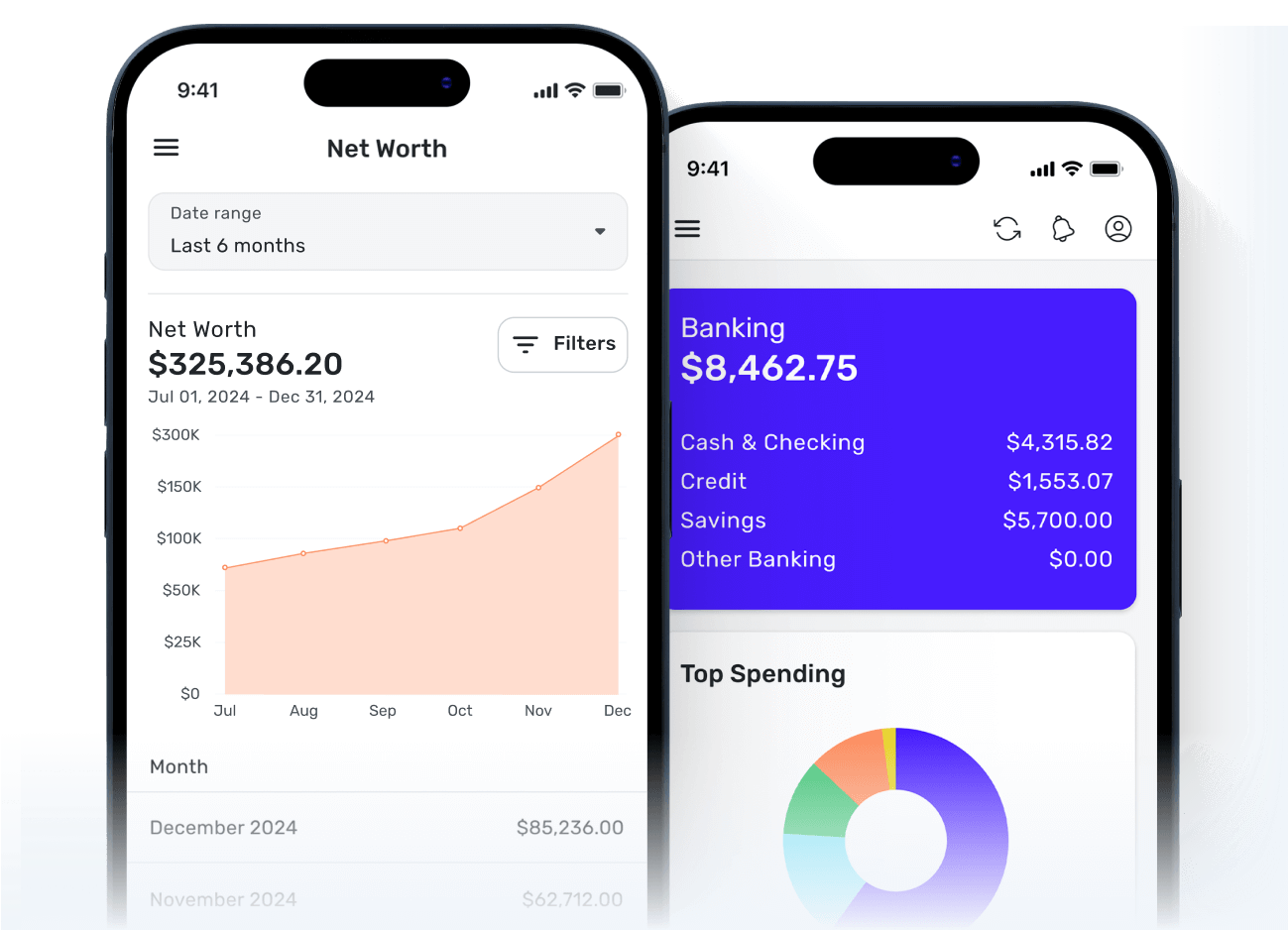

Connect & track all your accounts

Sync and manage your financial info from 14,000+ financial institutions.

Customers for over 40 years

Best Mint Alternative

Best budgeting app

Best personal finance app

Understand spending habits

Manage subscriptions

Save more

Pay down debt faster

Grow investments

Improve net worth

Manage cashflow

Get paid faster

Connect & track all your accounts

Sync and manage your financial info from 14,000+ financial institutions.

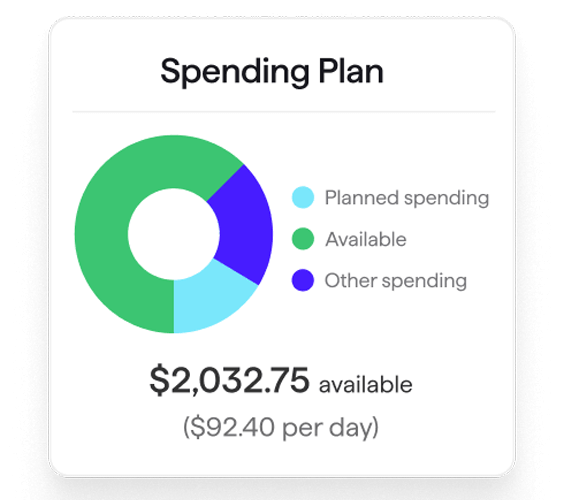

Spend & save with confidence

No matter your budget or savings goals, dial them in with Quicken

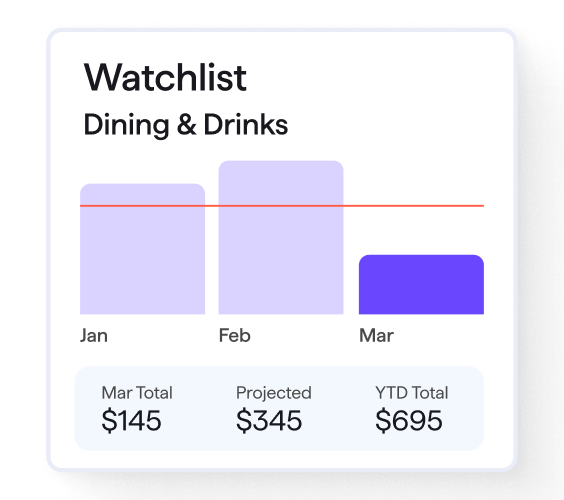

Tap into insights you can act on

Generate future-focused reports and analyses for smarter decisions.

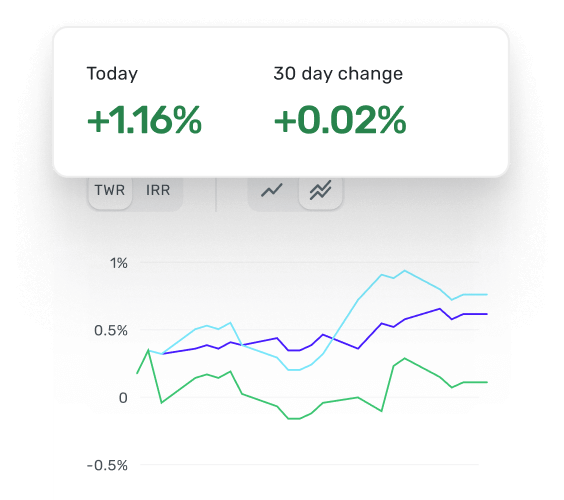

Build the future you want

Manage investments, retirement plans, and your entire portfolio.

Quicken Simplifi

Mobile

Web app

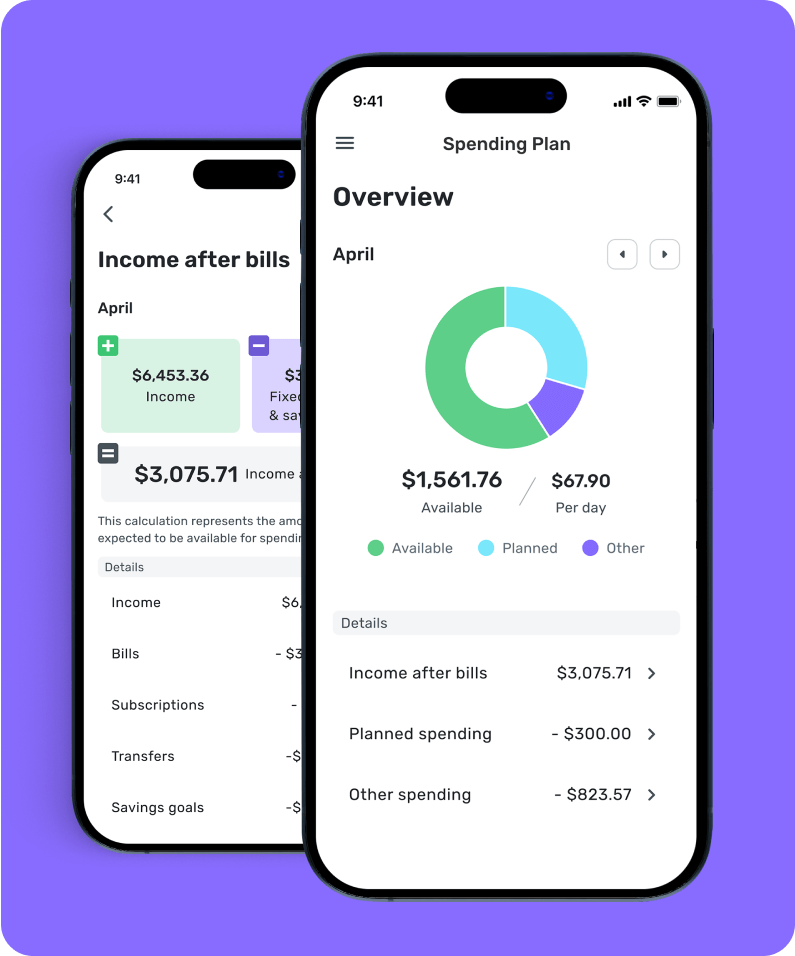

Always know what you have left to spend or save

Get better insights with reports & real-time alerts

Make informed decisions about your investment portfolio

Plan for the future with projected cash flows

Always know what you have left to spend or save

Get better insights with reports & real-time alerts

Make informed decisions about your investment portfolio

Plan for the future with projected cash flows

Quicken Business & Personal

Mobile

Web app

Manage business & personal finances in one app

Track cash flow with detailed performance reports

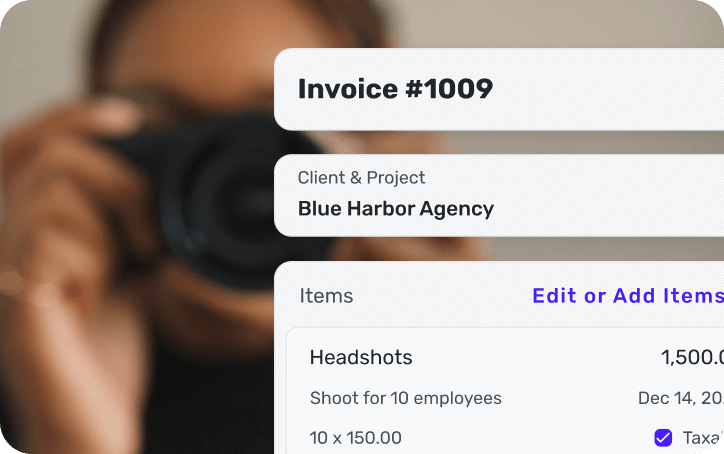

Use invoicing tools to get you paid faster

Simplify tax time with built-in Schedules C & E

Classic Premier

Windows

Mac

Best-in-class investing tools

Track the performance and optimize your investment portfolio

Set budgets, manage debt, create a retirement plan

Track & pay bills in Quicken

Best-in-class investing tools

Track the performance and optimize your investment portfolio

Set budgets, manage debt, create a retirement plan

Track & pay bills in Quicken

Classic Business & Personal

Windows

Mac

Manage business, personal, & rental finances

Stay on track with reports: cash flow, P&L, tax schedules, & more

Create customized invoices

Track portfolio performance & optimize your investing

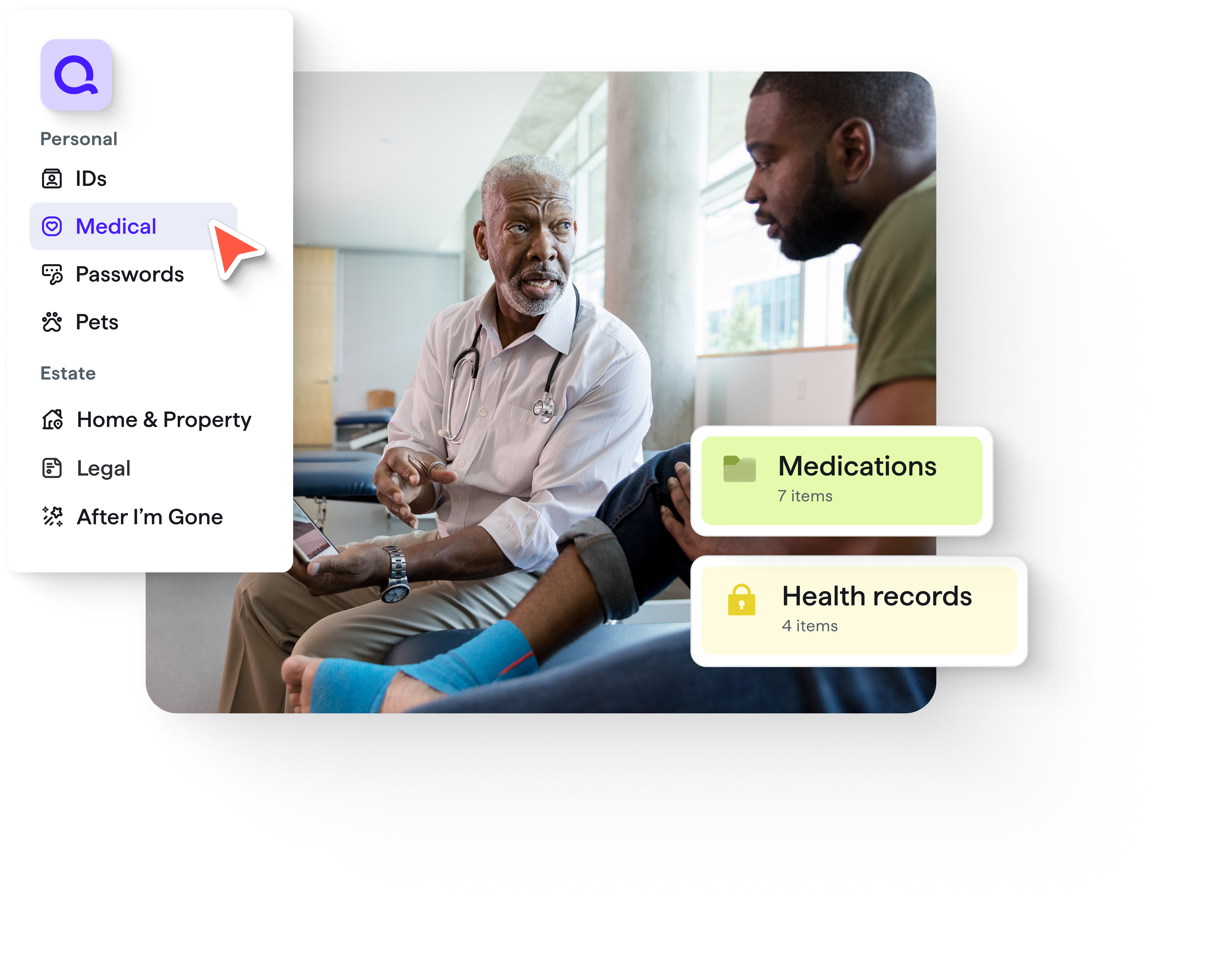

Always be ready for life’s big events, emergencies, and everyday moments. Keep vital info safe, secure, and shareable.

Trusted for over 40 years

#1 best-selling with 20+ million customers over 4 decades.

Bank-grade security

We protect your data with industry-standard 256-bit encryption.

Your privacy matters

Rest assured, we’ll never sell your personal data.

No surprise charges or ads

No hidden fees or annoying ads. What you see is what you get.